Physical Climate Risk vs Transition Risk: A Complete Industry Guide

- C² Team

- Mar 14

- 12 min read

How TCFD Defines the Two Faces of Climate Risk and What They Mean for Your Business

Climate risk is one of the most used and least precisely understood terms in corporate sustainability. It appears in board presentations, investor questionnaires, regulatory filings, and annual reports with a frequency that has grown dramatically as frameworks like the Task Force on Climate-related Financial Disclosures have moved from voluntary best practice to regulatory expectation across major economies. Yet in many organisations, the term is still being used as though it describes a single, unified category of risk, when in reality it describes two fundamentally different types of exposure that require different analytical frameworks, different data inputs, and different strategic responses.

The Task Force on Climate-related Financial Disclosures, established by the Financial Stability Board in 2015 and now embedded in regulatory requirements across the European Union, United Kingdom, United States, and many other jurisdictions, is explicit on this point. TCFD identifies two distinct categories of climate-related risk: physical risk, which arises from the direct physical impacts of climate change on assets, operations, and supply chains, and transition risk, which arises from the financial consequences of the global economy's shift toward a lower-carbon model. Both are mandatory subjects of scenario analysis and disclosure under TCFD. Both are material to business strategy and financial performance. And the strategies that reduce exposure to one can, in some circumstances, increase exposure to the other.

Understanding both categories in depth, and understanding how they manifest differently across sectors, is the foundation of any credible TCFD-aligned climate risk assessment.

Physical Climate Risk - When the Climate Itself Is the Threat

Physical climate risk encompasses the direct financial consequences of changes in climate patterns and the increasing frequency and severity of extreme weather events. TCFD subdivides physical risk into two types that operate on different timescales and through different mechanisms.

Acute physical risks are event-driven. They arise from discrete extreme weather events whose probability and severity are increasing as global average temperatures rise. Floods, cyclones, tropical storms, wildfires, extreme heat events, and severe droughts are all examples of acute physical risks. Their financial consequences can be sudden and severe, including direct asset damage, business interruption, supply chain disruption, and emergency response costs. The increasing frequency and intensity of these events is now well-documented in the scientific literature, and the insurance sector, which absorbs much of the financial cost of acute physical events, has been tracking the trend in insured losses for decades.

Chronic physical risks operate over longer timescales and arise from sustained shifts in climatic conditions rather than discrete events. Rising sea levels, increasing average temperatures, changing rainfall patterns, permafrost thaw, and shifts in seasonal cycles are all examples of chronic physical risks. Their financial consequences tend to materialise more gradually than those of acute events, but they can be equally or more significant in aggregate, particularly for assets and operations with long useful lives or for business models whose economics are dependent on stable climatic conditions.

The assessment of physical climate risk requires scenario analysis using climate science projections under different global warming trajectories, typically the Representative Concentration Pathways defined by the Intergovernmental Panel on Climate Change. A physical risk assessment under a 1.5 degree scenario will produce different findings from one conducted under a 3 or 4 degree scenario, and the difference between those scenarios is not merely one of degree but of fundamental changes in the nature, location, and severity of risks that businesses face.

Transition Risk - When the Response to Climate Change Is the Threat

Transition risk is a different beast entirely. It does not arise from changes in the physical climate but from the financial and economic consequences of the global response to climate change. As governments, regulators, investors, customers, and civil society act to reduce greenhouse gas emissions and accelerate the shift to a lower-carbon economy, businesses that are exposed to high-emission activities, technologies, or business models face financial risks that can be equally material to those arising from physical impacts.

TCFD identifies four subcategories of transition risk that together cover the main channels through which the low-carbon transition creates financial exposure.

Policy and legal risk encompasses the financial consequences of climate-related regulatory changes and litigation. Carbon pricing mechanisms, emission performance standards, mandatory disclosure requirements, sector-specific emission reduction targets, and bans on particular technologies or fuels all create policy risk for businesses exposed to the affected activities. Legal risk arises from litigation related to climate change, including claims against companies for failing to disclose material climate risks, for misrepresenting their climate credentials, or for contributing to climate damages.

Technology risk arises from the disruption created by the development and deployment of lower-carbon technologies. When renewable energy reaches cost parity with fossil fuel generation, when electric vehicles reach purchase price parity with internal combustion engine vehicles, or when green hydrogen becomes cost-competitive with grey hydrogen, incumbent technologies face accelerating displacement. The assets, skills, and business models built around those incumbent technologies face impairment as the transition accelerates.

Market risk encompasses shifts in supply and demand driven by changing preferences, changing input costs, and changing availability of capital. As investors integrate climate considerations into their allocation decisions, as consumers shift purchasing behaviour in response to climate concerns, and as commodity markets reprice in response to the energy transition, businesses face market risk that can affect both their revenues and their cost structures.

Reputational risk arises from the perception held by customers, investors, employees, regulators, and civil society of a company's response to climate change. Companies perceived as laggards on climate, as greenwashers, or as active opponents of climate policy face reputational consequences that can translate into lost customers, difficulty attracting talent, higher cost of capital, and regulatory scrutiny. As climate commitments made by companies become subject to increasing external verification and accountability, the gap between claimed and actual climate performance is becoming a material source of reputational exposure.

Physical and Transition Risk by Industry

The relative weight of physical and transition risk varies significantly across sectors, as does the specific form those risks take. The following industry-level analysis illustrates how both risk categories manifest in practice across different parts of the economy.

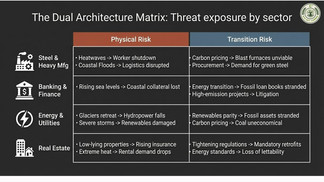

Steel and Heavy Manufacturing

For steel producers and heavy manufacturers, physical climate risk is concentrated in the vulnerability of fixed industrial assets and supply chains to extreme weather events and chronic climate shifts. Manufacturing facilities located in flood plains, coastal zones, or areas subject to increasing water stress face growing exposure to operational disruption from both acute flood events and chronic water availability constraints. Extreme heat events pose a direct operational risk in facilities where outdoor work is a significant component of operations, as heat thresholds that trigger mandatory work stoppages are being exceeded with increasing frequency in many industrial geographies. Supply chain physical risk is equally significant, as the raw materials flowing into heavy manufacturing, including iron ore, coking coal, bauxite, and agricultural inputs for bio-based materials, are themselves sourced from geographies with significant physical climate exposure.

Transition risk for steel and heavy manufacturing is among the most acute of any industrial sector. The steel industry alone accounts for approximately 7% of global greenhouse gas emissions, and the carbon intensity of conventional blast furnace and basic oxygen furnace steelmaking makes it a primary target of carbon pricing mechanisms, emission performance standards, and green procurement requirements. The introduction of the European Union Carbon Border Adjustment Mechanism, which applies a carbon price to imports of steel, cement, aluminium, fertilisers, electricity, and hydrogen into the EU market, represents a structural shift in the competitive economics of high-emission industrial production. For steel producers in jurisdictions without equivalent carbon pricing, CBAM creates a direct market access risk that will intensify as the mechanism reaches full implementation. At the same time, the growing demand from automotive, construction, and consumer goods buyers for verified low-carbon or green steel is creating both a market risk for producers who cannot meet those specifications and a market opportunity for those who can.

Agriculture and Food

For agricultural producers and food companies, physical climate risk is direct, multidimensional, and already materialising in ways that are visible in commodity price volatility, crop yield data, and insurance markets. Shifting rainfall patterns are altering the geographic viability of key crops, with some regions experiencing increasing drought frequency and others experiencing flooding that destroys harvests and degrades soil. Rising average temperatures are compressing growing seasons in some regions, increasing pest and disease pressure, and reducing the productivity of livestock in heat-stressed environments. Water availability is a compounding physical risk for irrigated agriculture, as changing precipitation patterns and glacier retreat reduce the reliability of water supplies in regions that are critical for global food production.

Chronic physical risks in agriculture extend beyond the farm gate into the processing, storage, and distribution infrastructure of the food supply chain. Extreme heat affects cold chain integrity, storage facility operating costs, and the shelf life of perishable products. Flooding disrupts logistics networks and can contaminate food processing facilities. The financial consequences of physical climate risk in agriculture are already being priced into commodity futures markets and agricultural insurance products, with implications that flow through to the entire food value chain.

Transition risk for agriculture and food manifests primarily through regulatory and market channels. Methane emission regulations targeting livestock production are tightening in multiple jurisdictions and are likely to impose compliance costs on producers of beef, dairy, and other ruminant livestock products. Nitrogen and synthetic fertiliser regulations are evolving in response to both climate and biodiversity concerns, creating transition risk for input-intensive production systems. On the market side, the shift in consumer demand toward lower-carbon and plant-based food products represents a long-term structural transition risk for companies with business models centred on high-emission animal protein, and a corresponding opportunity for those investing in alternative protein development and lower-carbon agricultural systems.

Banking and Financial Services

For banks, insurers, asset managers, and other financial institutions, both physical and transition risk operate primarily through the portfolio rather than through direct operational exposure. The physical climate risk embedded in a financial institution's balance sheet is a function of the physical risk exposure of its borrowers, investees, and insured parties. Mortgage portfolios secured against coastal or flood-prone residential property carry physical risk that materialises as collateral value impairment and increased default rates as physical climate impacts affect property values and insurability. Commercial real estate lending in climate-exposed geographies carries similar risks. Agricultural lending and trade finance linked to climate-sensitive commodity supply chains carries physical risk that can affect credit quality as climate events disrupt production and commodity flows.

The transition risk in financial institution portfolios is centred on the exposure to high-emission assets and business models that face impairment as the low-carbon transition accelerates. Lending to fossil fuel producers, high-emission industrial companies, and carbon-intensive real estate carries transition risk that is increasingly being scrutinised by prudential regulators, who are requiring banks to conduct climate scenario analysis of their loan books and to assess the impact of different transition pathways on credit quality and capital adequacy. The Network for Greening the Financial System has developed standardised climate scenarios that central banks and supervisors use to assess the systemic climate risk implications of different transition speeds, and individual institutions are required under frameworks such as the European Central Bank's climate risk supervisory expectations to integrate these scenarios into their own risk management frameworks.

Legal risk is a growing dimension of transition risk for financial institutions, as litigation against banks and investors for financing high-emission projects, for making misleading sustainability claims, and for failing to disclose material climate risks to clients and beneficiaries is increasing in volume and sophistication across multiple jurisdictions.

Energy and Utilities

The energy sector sits at the intersection of physical and transition risk in ways that make climate risk assessment particularly complex and consequential. For fossil fuel producers and thermal power generators, transition risk is the dominant concern. The accelerating deployment of renewable energy, the falling cost trajectory of battery storage, the introduction and tightening of carbon pricing mechanisms, and the growing availability of green hydrogen all threaten to erode the economic viability of fossil fuel assets on timescales that are much shorter than their engineering lifespans. Stranded asset risk, meaning the risk that productive assets must be written down or written off before the end of their economic life due to changes in the regulatory, market, or technological environment, is the defining transition risk for the fossil fuel energy sector.

Physical risk for energy infrastructure is equally significant and operates across both acute and chronic dimensions. Hydropower generation is directly vulnerable to changes in precipitation patterns and glacier retreat that affect river flows and reservoir levels. The reliability and capacity of hydropower assets in water-stressed regions is already declining in some cases and is projected to decline further under higher warming scenarios. Thermal power stations that rely on river or coastal water for cooling face operational constraints during extreme heat events when water temperatures rise above regulatory thresholds or water flows fall below minimum levels. Offshore wind and coastal energy infrastructure faces increasing exposure to storm damage as cyclone intensity increases. Electricity transmission and distribution networks face increasing exposure to wildfire, flooding, and extreme heat events that cause outages and infrastructure damage.

For renewable energy developers and utilities transitioning their asset portfolios, transition risk is primarily an opportunity rather than a threat, but physical risk remains a significant consideration in asset siting, design standards, and long-term revenue projections.

Real Estate

For real estate investors, developers, and operators, physical climate risk is increasingly a first-order financial concern rather than a long-term theoretical consideration. The repricing of flood risk in coastal and riverine property markets is already visible in insurance premium data, with some properties in high-risk locations becoming uninsurable or prohibitively expensive to insure. As insurance availability contracts and premiums rise, the investment case for affected properties deteriorates, lender appetite diminishes, and asset values face structural pressure. Rising sea levels compound flood risk over longer timescales, threatening the permanent inundation of low-lying coastal assets in scenarios consistent with current emission trajectories.

Extreme heat poses a chronic physical risk to the liveability and economic productivity of urban real estate in warm climate zones. As heat island effects intensify in dense urban environments and as the frequency of days exceeding critical heat thresholds increases, the demand for office space, retail premises, and residential property in affected locations is likely to be affected. The energy costs associated with cooling are also a significant operational risk for commercial property in heat-stressed geographies.

Transition risk in real estate is concentrated in the energy performance of the existing building stock. Tightening minimum energy performance standards in multiple jurisdictions are creating a regulatory transition risk for properties that do not meet or cannot cost-effectively be upgraded to meet the required standards. In the United Kingdom, the trajectory of Minimum Energy Efficiency Standards regulations for commercial property signals that buildings below an Energy Performance Certificate rating of B may face significant lettability restrictions in the medium term. Across the European Union, the Energy Performance of Buildings Directive is driving similar requirements. The capital expenditure required to retrofit existing buildings to meet these standards, and the risk of stranded asset value for properties where retrofitting is not technically or economically viable, represents a material transition risk for real estate portfolios with significant exposure to older, low-efficiency stock.

Why TCFD Requires Both Lenses Simultaneously

The TCFD framework does not allow companies to choose between physical and transition risk analysis. It requires both, and for good reason. The two risk categories are not simply additive but can interact in complex and sometimes counterintuitive ways that only become visible when both are assessed simultaneously.

A company that responds to transition risk by rapidly decarbonising its operations and investing in new low-carbon production technology may reduce its regulatory and market exposure significantly. But if the new facilities in which it invests are located in geographies with high physical climate exposure, the transition risk reduction may be accompanied by an increase in physical risk that partially or wholly offsets the strategic benefit. A financial institution that reduces its transition risk by divesting from fossil fuel assets may increase its concentration in real estate or agricultural lending that carries significant physical risk. An energy company that invests heavily in offshore wind to reduce its transition risk profile must simultaneously manage the physical risk that increasingly severe storms pose to those offshore assets.

TCFD's scenario analysis requirement is designed to surface these interactions by requiring companies to assess their risk profile under multiple climate scenarios that differ in both the speed of the low-carbon transition and the degree of physical warming that results. A fast transition scenario, such as one consistent with a 1.5 or well below 2 degree pathway, implies high transition risk in the near term but lower physical risk over the long term as warming is limited. A slow transition scenario implies lower near-term transition risk but significantly higher long-term physical risk as warming trajectories approach 3 or 4 degrees. The full picture of a company's climate risk profile only becomes visible when it is assessed across this range of scenarios rather than optimised for a single assumed future.

Building a Credible TCFD-Aligned Risk Framework

For companies moving from awareness of physical and transition risk to a credible and operational TCFD-aligned risk framework, the practical requirements are substantial but well-defined.

The first requirement is scenario selection. TCFD recommends using at least two scenarios, one consistent with a well-below-2-degree pathway and one representing a higher warming trajectory. The scenarios developed by the Network for Greening the Financial System are widely used as a reference point, as are those published by the International Energy Agency. The selection of scenarios should be documented and justified, and the assumptions embedded in each scenario should be clearly disclosed.

The second requirement is risk identification and assessment across both physical and transition risk categories, for all relevant geographies, time horizons, and business segments. This requires integrating climate science data into the physical risk assessment and policy, technology, and market analysis into the transition risk assessment, at a level of specificity that is sufficient to inform strategic decision-making rather than merely satisfying a disclosure checklist.

The third requirement is financial quantification. TCFD expects companies to articulate the potential financial impact of identified risks and opportunities, even where precise quantification is not yet possible. This requires integrating climate risk findings into financial modelling frameworks and making explicit the assumptions and uncertainties involved.

The fourth requirement is strategic integration. Climate risk findings that remain in a sustainability report annexe and do not influence capital allocation, investment decisions, asset management strategy, or risk appetite frameworks are not meeting the spirit of TCFD, even if they satisfy the letter. The ultimate purpose of the framework is to ensure that climate risk is managed with the same rigour and strategic seriousness as any other category of material financial risk.

Climate risk is not one risk. It is two, operating through different mechanisms, on different timescales, and requiring different responses. Companies that understand both, assess both rigorously, and integrate both into their strategic planning are building the climate resilience that regulators, investors, and stakeholders are increasingly demanding and that the physical and economic realities of the coming decades will require.

👉 Connect with C² (Csquare) to get started!

🌐 csquarecarbon.com

✉️ info@csquare.co.in

Comments