I-RECs vs RECs vs Carbon Credits: When to Use Which

- C² Team

- Feb 26

- 12 min read

I-RECs vs RECs vs Carbon Credits: When to Use Which

Published by Csquare (C2) | csquarecarbon.com

Most companies entering the sustainability space encounter three instruments almost simultaneously: I-RECs, RECs, and Carbon Credits. On the surface they can appear similar. They are all market-based. They all come with certificates. They are all associated with climate and energy claims. And yet they serve entirely different purposes, operate under different standards, and cannot be substituted for one another.

Using the wrong instrument for a particular claim does not just create a gap in your ESG reporting. It creates a liability. Investors, ESG rating agencies, and increasingly sophisticated regulators are scrutinizing corporate claims more rigorously than ever before. Understanding exactly what each instrument does, what it proves, and when to use it is no longer optional for Indian companies with sustainability commitments. It is a baseline competency.

This blog provides a comprehensive, practical breakdown of all three instruments, with particular attention to the Indian regulatory and market context.

1. The Foundational Principle: These Are Not Substitutes

Before examining each instrument individually, the most important principle to establish is this: I-RECs, RECs, and Carbon Credits measure different things and address different types of corporate sustainability claims. They cannot replace one another. Purchasing carbon credits does not entitle a company to claim renewable energy use. Purchasing RECs does not allow a company to offset its total greenhouse gas emissions.

The confusion typically arises because all three instruments are traded in market-based systems and are associated with environmental outcomes. But the outcome each one represents is distinct:

• RECs and I-RECs answer the question: Where did our electricity come from? They prove that a quantity of electricity was generated from a renewable source.

• Carbon Credits answer the question: How much have we reduced or compensated for our greenhouse gas emissions? They prove that a tonne of CO2 equivalent was avoided, reduced, or removed from the atmosphere.

Getting this distinction right is the first step to building a credible sustainability strategy.

2. Understanding RECs: India's Domestic Renewable Energy Certificate

What Is a REC?

A Renewable Energy Certificate (REC) in India is a market-based instrument that represents the environmental attributes of 1 MWh of electricity generated from a renewable energy source such as solar, wind, small hydro, or biomass. RECs were introduced in India through Central Electricity Regulatory Commission (CERC) regulations in 2010 and trading began on the Indian Energy Exchange (IEX) and Power Exchange India Limited (PXIL) in 2011.

The fundamental concept is a separation of the electricity commodity from its environmental attributes. When a renewable energy plant generates power, it can sell the electricity itself into the grid at conventional tariffs and separately issue a REC for each MWh generated. A company that purchases that REC can then claim that 1 MWh of its electricity consumption was matched by renewable generation, even if it is not physically connected to that plant.

The Regulatory Architecture

RECs in India sit within a compliance-driven framework. The Renewable Purchase Obligation (RPO) mandates that certain categories of electricity consumers, including distribution companies, open access consumers, and captive power users above a specified threshold, source a defined percentage of their electricity from renewable sources. RPO targets are set by CERC and State Electricity Regulatory Commissions (SERCs) and are being progressively raised, with the central government setting an RPO trajectory that reaches 43.33% by 2029-30.

Companies that cannot meet their RPO through physical renewable energy procurement can purchase RECs to demonstrate compliance. This makes RECs the only one of the three instruments with a direct regulatory compliance function in India.

Voluntary Use of RECs

Beyond compliance, companies can purchase RECs voluntarily to support their renewable energy claims in ESG reporting. Under the GHG Protocol Scope 2 Guidance, market-based accounting allows companies to use the emissions factor of the electricity they have contractually sourced rather than the grid average. A REC purchased for a specific period of generation allows a company to claim zero emissions for the corresponding quantity of electricity under the market-based method.

However, this claim is limited strictly to electricity. RECs do not address Scope 1 emissions from fuel combustion, Scope 3 emissions from supply chains, or any non-electricity energy use such as diesel for transport or gas for heating.

Key point for Indian companies: If you have an RPO obligation, RECs are both a compliance tool and an ESG reporting tool. If you do not have an RPO obligation but want to make a renewable electricity claim, RECs serve the same purpose on a voluntary basis. In either case, RECs only address electricity. |

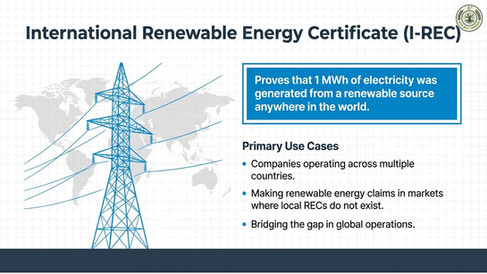

3. Understanding I-RECs: The International Standard for Cross-Border Claims

What Is an I-REC?

An International Renewable Energy Certificate (I-REC) is functionally equivalent to a domestic REC but operates under an internationally standardized framework governed by the I-REC Standard, now part of EnergyTag. Each I-REC represents 1 MWh of renewable electricity generation and is issued, tracked, and retired through a centralized registry that operates across more than 50 countries.

The key distinction from a domestic REC is the international portability and standardization. An I-REC issued for solar generation in Rajasthan can be purchased and retired by a company headquartered in the Netherlands as part of its global renewable energy claim. This makes I-RECs the instrument of choice for multinational companies that need to make renewable energy claims across markets where local certificate systems either do not exist or are not internationally recognized.

Why I-RECs Matter for Indian Companies

For Indian companies, I-RECs are relevant in two important contexts. First, Indian subsidiaries or affiliates of multinational corporations may be required to report renewable energy consumption using I-RECs to align with the parent company's global RE100 or SBTi commitments. Global frameworks like RE100 specify that renewable energy claims must be backed by certificates that meet certain quality criteria, and I-RECs generally satisfy these requirements where domestic RECs may not always be accepted.

Second, Indian renewable energy generators can register their plants under the I-REC Standard and issue I-RECs for export to global buyers. This creates an additional revenue stream for Indian renewable energy producers and helps channel international sustainability capital into India's clean energy sector.

I-RECs and RPO Compliance

It is important to note that I-RECs are currently not recognized for RPO compliance purposes in India. If a company has a mandatory RPO obligation under Indian regulations, it must use domestic RECs traded on recognized Indian power exchanges. I-RECs serve voluntary and international reporting purposes only within the Indian regulatory context.

4. Understanding Carbon Credits: The Instrument for Emissions Accounting

What Is a Carbon Credit?

A carbon credit represents 1 metric tonne of carbon dioxide equivalent (tCO2e) that has been avoided, reduced, or removed from the atmosphere. Carbon credits can be generated by a wide range of project types including renewable energy projects, methane capture, cookstove programs, reforestation and afforestation, soil carbon sequestration, blue carbon initiatives such as mangrove conservation, and direct air capture technologies.

Unlike RECs and I-RECs, which are always tied to electricity generation, carbon credits can originate from any sector and address any source of emissions. This makes them a far more versatile instrument for companies seeking to account for their total greenhouse gas footprint rather than just their electricity consumption.

Voluntary vs Compliance Carbon Markets

Carbon markets operate in two distinct categories. Compliance markets are mandatory, government-operated systems such as the European Union Emissions Trading System (EU ETS) or China's national carbon market, where regulated entities must surrender credits to cover their reported emissions. India's own carbon market, the Carbon Credit Trading Scheme (CCTS) announced by the Bureau of Energy Efficiency, is being developed as a compliance market for designated industries.

Voluntary carbon markets allow companies to purchase credits outside of any regulatory obligation, typically to support net zero commitments, offset residual emissions, or fund climate projects as part of an ESG or CSR strategy. The voluntary market is governed by independent standards such as Verra's Verified Carbon Standard (VCS), the Gold Standard, the American Carbon Registry, and others. Credits under these standards must demonstrate additionality, permanence, and independent third-party verification.

The Role of Carbon Credits in a Net Zero Strategy

Carbon credits are not a replacement for emissions reduction. The Science Based Targets initiative (SBTi) and other leading frameworks are explicit that companies must prioritize deep decarbonization of their own operations and value chains. Carbon credits are used to compensate for residual emissions that cannot yet be eliminated, particularly in hard-to-abate sectors, or to demonstrate progress while longer-term reduction pathways are being implemented.

The quality of a carbon credit matters enormously. Credits differ significantly in terms of the permanence of the underlying outcome, the rigor of the methodology, the vintage year, and co-benefits for local communities and biodiversity. A cheap credit from a poorly designed project is not equivalent to a high-integrity credit from a rigorously verified one, and the market and regulators are increasingly able to tell the difference.

Important distinction: Carbon credits from renewable energy projects do exist, but a company cannot use the same activity to generate both a REC and a carbon credit. This is called double counting and is explicitly prohibited under all major standards. A renewable energy generator must choose whether to issue RECs or carbon credits for a given unit of generation, not both. |

5. Side-by-Side Comparison

The table below summarizes the key attributes of all three instruments:

Attribute | I-REC | REC (India) | Carbon Credit |

What it measures | 1 MWh of renewable electricity generated | 1 MWh of renewable electricity generated | 1 tonne of CO2e avoided, reduced, or removed |

Scope addressed | Scope 2 (market-based) | Scope 2 (market-based) | Scope 1, 2, and 3 |

Geography | Global, cross-border | Country-specific (India: IEX) | Global |

Governing body | EnergyTag / I-REC Standard | Central Electricity Regulatory Commission (CERC) | Gold Standard, Verra (VCS), CDM |

Indian regulatory link | Voluntary, no RPO credit | Valid for RPO compliance | Voluntary (no domestic mandate yet) |

Used to claim | Renewable energy sourcing | Renewable energy sourcing / RPO | Carbon neutrality / Net Zero |

Can offset GHG emissions? | No | No | Yes |

Interchangeable? | Not with carbon credits | Not with carbon credits | Not with RECs or I-RECs |

Market maturity in India | Growing, used by MNCs | Established since 2011 | Growing, voluntary |

Typical buyer | Multinationals, RE100 members | Obligated entities, ESG-driven companies | Companies with Net Zero targets |

6. Common Mistakes Indian Companies Make

Despite the clear distinctions between these instruments, several recurring errors appear in corporate sustainability reporting across Indian companies:

Using Carbon Credits to Claim Renewable Energy Use

Some companies purchase carbon credits from renewable energy projects under the assumption that this gives them the right to claim renewable electricity. It does not. A carbon credit documents a reduction in greenhouse gas emissions. It does not transfer the renewable energy attribute of the underlying electricity generation. The GHG Protocol is explicit on this point, and RE100 and CDP disclosures require instrument-specific claims.

Treating RECs as Offsets for Total Emissions

RECs address Scope 2 electricity emissions only when used in market-based accounting. They do not offset Scope 1 fuel combustion, Scope 3 supply chain emissions, or any other emission source. A company that purchases RECs for all of its electricity consumption has not offset its total carbon footprint. It has only addressed one component of it.

Double Counting

Companies that generate or purchase renewable energy through power purchase agreements (PPAs) sometimes also purchase RECs or I-RECs for the same electricity. This constitutes double counting. If a renewable energy attribute has already been transferred through a PPA at a bundled premium, a separate REC cannot be claimed for that same generation.

Using Expired or Low-Quality Credits

Both carbon credits and RECs have vintage years. Using credits from many years prior to the reporting period is increasingly challenged by auditors and rating agencies. Some carbon credits also carry significant integrity risks, particularly those from projects with weak additionality arguments or unverified permanence. The Voluntary Carbon Markets Integrity Initiative (VCMI) and the Integrity Council for the Voluntary Carbon Market (ICVCM) are developing quality standards that investors and ESG agencies will use to evaluate credit portfolios.

Confusing I-RECs with Carbon Offsets for Scope 2

Under the GHG Protocol Scope 2 Guidance, there are two methods for calculating Scope 2 emissions. The location-based method uses the average grid emissions factor. The market-based method uses the emissions factor of the electricity a company has contractually sourced. I-RECs and RECs are instruments used under the market-based method to claim a zero or renewable emissions factor. They are not carbon offsets in the traditional sense, even though their net effect on a Scope 2 calculation may appear similar.

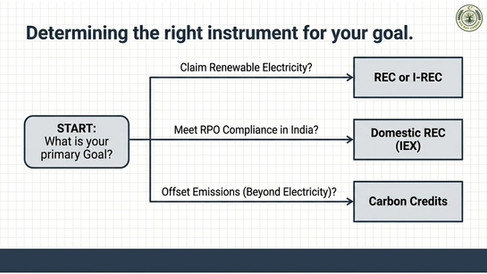

7. When to Use Each Instrument: A Decision Framework

The following framework provides a practical guide for Indian companies determining which instrument is appropriate for their needs:

Use Domestic RECs When:

• You have a mandatory RPO compliance obligation under Indian regulations

• You want to make a renewable electricity claim for domestic operations reported under Indian ESG frameworks such as BRSR

• Your reporting is primarily domestic and you do not need international portability

• You want to support India's renewable energy market through a well-established, regulated instrument

Use I-RECs When:

• You are a multinational or Indian subsidiary of a global company that needs to make renewable energy claims across multiple geographies

• Your parent company is a RE100 member and requires internationally recognized certificate formats

• You are reporting to CDP and require certificates that meet CDP's quality criteria for market-based Scope 2 accounting

• You operate in markets where no domestic certificate system exists and need a standardized alternative

Use Carbon Credits When:

• You need to address Scope 1 emissions from fuel combustion, industrial processes, or refrigerant leakage

• You need to address Scope 3 emissions from supply chains, business travel, logistics, or purchased goods and services

• You are pursuing a carbon neutrality or net zero claim that requires accounting for your total GHG footprint beyond just electricity

• You are building a carbon offset portfolio as part of a broader climate strategy aligned with SBTi or similar frameworks

• You want to contribute to specific climate projects such as forest conservation, clean cooking, or methane reduction

Practical rule of thumb: If your sustainability question starts with electricity, use a REC or I-REC. If it starts with emissions, use carbon credits. If your question involves both, you likely need both, applied correctly to each. |

8. The Indian Market Landscape

REC Market in India

India's REC market has been operational since 2011 and is overseen by the CERC. RECs are issued by the National Load Despatch Centre (NLDC) and traded on the IEX and PXIL. The market underwent significant reforms in 2022 with CERC revising the REC framework to introduce a single category system removing the previous solar and non-solar distinction, setting new floor and forbearance price structures, and extending validity of unsold RECs. These reforms have improved market liquidity and broadened participation.

Trading volumes have grown substantially in recent years, driven by increasing RPO targets and greater voluntary demand from ESG-focused companies. Indian renewable energy generators ranging from large utility-scale solar and wind developers to smaller biomass and small hydro projects participate as REC issuers.

India's Emerging Carbon Market

India is in the process of establishing its domestic carbon market under the Energy Conservation (Amendment) Act 2022. The Carbon Credit Trading Scheme (CCTS), being developed by the Bureau of Energy Efficiency (BEE) under the Ministry of Power, will initially focus on designated industrial sectors with specific emissions intensities and will create a compliance framework for carbon trading within India.

In parallel, the voluntary carbon market in India has been growing, with Indian projects in forestry, agriculture, clean energy, and waste management generating credits for both domestic and international buyers. India is one of the largest suppliers of voluntary carbon credits globally, and this market is expected to deepen as domestic demand from Indian companies pursuing net zero targets increases.

I-RECs in the Indian Context

India is one of the largest I-REC-issuing countries globally, reflecting the scale and growth of its renewable energy sector. Indian renewable energy developers registered under the I-REC Standard can issue certificates that attract international buyers, particularly multinational corporations with operations in India seeking to meet global RE100 or SBTi-aligned targets. The I-REC market in India is currently dominated by solar and wind generation, reflecting the rapid expansion of these technologies.

9. Building a Coherent Instrument Strategy

For most Indian companies with meaningful sustainability commitments, a single instrument will not be sufficient. A robust and credible ESG strategy typically requires a combination of instruments applied correctly to different parts of the emissions inventory.

A company with operations across India and internationally might use domestic RECs to meet RPO compliance obligations, I-RECs for international subsidiaries reporting under RE100, and carbon credits to address Scope 1 and Scope 3 emissions as part of a net zero pathway. The key is ensuring that each instrument is applied to the right claim, that double counting is avoided, and that the overall strategy is supported by transparent disclosure.

The quality and integrity of instruments chosen also matters as much as the quantity. Low-quality carbon credits from projects with questionable additionality, or RECs from generators in grid zones with minimal renewable penetration, do not carry the same credibility as high-integrity alternatives. As investor scrutiny and third-party ESG assessments become more sophisticated, instrument quality will increasingly distinguish leaders from laggards.

1. Conduct a full GHG inventory covering Scope 1, 2, and 3 emissions to understand your total footprint and where each instrument type applies.

2. Map your compliance obligations, specifically identify whether you have RPO requirements under Indian law and ensure REC procurement is aligned.

3. Align with international frameworks if you are RE100, SBTi, or CDP-aligned, ensure your certificate choices meet those frameworks' quality and reporting requirements.

4. Prioritize reduction before offsetting, use instruments to complement your decarbonization pathway, not to replace it.

5. Work with specialists who understand both the Indian regulatory environment and international standards to ensure your instrument mix is accurate, credible, and defensible.

Conclusion: Precision Is a Competitive Advantage

The market for sustainability instruments is maturing rapidly. A few years ago, purchasing any form of renewable energy certificate or carbon credit was seen as progressive. Today, the question is not whether a company has purchased these instruments but whether it has used them correctly, applied them to the right claims, sourced them from credible projects, and reported them transparently.

Indian companies that take the time to understand the precise function of I-RECs, RECs, and Carbon Credits, and build strategies that use each instrument for its intended purpose, will not only avoid the growing risk of greenwashing allegations. They will build the kind of credible, defensible sustainability narrative that attracts long-term investors, satisfies global buyers, and positions them competitively in a world where environmental performance is increasingly priced into capital and commercial relationships.

Getting the instruments right is not the end of the sustainability journey. But it is a necessary foundation for everything that follows.

The question is not just what you buy. It is whether what you buy proves what you claim.

Connect with C2 (Csquare) to Get Started

Csquare is India's specialist in carbon and renewable energy finance. We help companies navigate REC compliance, design credible carbon credit portfolios, align with global standards, and build ESG reporting frameworks that stand up to investor and regulatory scrutiny.

Website: csquarecarbon.com

Email: info@csquare.co.in

Comments