FMCG Supply Chain: Where 80% of Your Emissions Hide

- C² Team

- Feb 28

- 8 min read

Why Packaging, Distribution, and Retail Are the Real Climate Frontier for Consumer Goods Companies

Walk through the sustainability report of almost any major FMCG company and you will find detailed disclosures about factory energy consumption, on-site renewable energy installations, and manufacturing process improvements. These are presented as evidence of a serious commitment to reducing carbon emissions, and in isolation they are not wrong. Operational efficiency matters. Cleaner manufacturing processes matter.

But they represent, at most, 20% of the picture.

For the vast majority of fast-moving consumer goods companies, the remaining 80% of their carbon footprint sits outside the factory gates entirely. It sits in the packaging that wraps every product, the trucks and ships that move those products across thousands of kilometres, and the retail environments where consumers ultimately find them. These are the areas where the real climate accountability lies, and they are the areas that most FMCG sustainability strategies have historically underserved.

Understanding why requires a clear-eyed look at each of these three domains.

Packaging - The Carbon in Every Product Before It Reaches a Customer

Packaging is one of the most consequential and least interrogated sources of emissions in the FMCG value chain. For most consumer goods companies, packaging sits within Scope 3 Category 1, purchased goods and services, and represents a significant share of the total embodied carbon in their products. Yet in the majority of organisations, packaging decisions are made primarily on the basis of cost, shelf appeal, and product protection, with carbon impact treated as a secondary consideration at best.

The carbon story of packaging begins long before it reaches a retail shelf. It starts with the extraction of raw materials, whether that is petroleum for plastic production, wood pulp for paper and cardboard, bauxite for aluminium, or silica sand for glass. Each of these extraction and processing chains carries a substantial carbon cost that is entirely upstream of the FMCG company's own operations but entirely within its Scope 3 footprint.

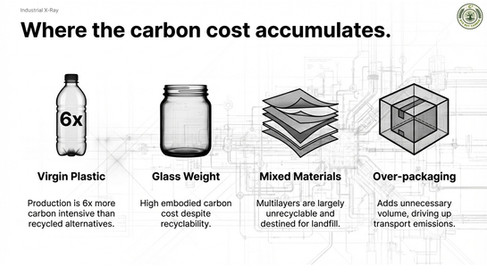

Virgin plastic production is approximately six times more carbon intensive than producing the same plastic from recycled feedstock. Despite this, virgin plastic continues to dominate packaging across most FMCG categories, driven by cost, availability, and the performance requirements of food safety and product shelf life. Glass packaging, while widely perceived as a sustainable alternative due to its recyclability, carries a significant embodied carbon burden in its production and is considerably heavier than plastic alternatives, which increases transport emissions throughout the distribution chain.

Multilayer and mixed-material packaging presents a particular challenge. Many high-barrier food and personal care packaging formats combine multiple materials, such as plastic, foil, and paper, in ways that make them technically unrecyclable under current infrastructure. These formats protect product quality and extend shelf life, which has genuine sustainability benefits in terms of food waste reduction, but they also contribute to a growing stream of packaging waste that ends up in landfill or incineration rather than being recovered and reused.

The carbon cost of packaging does not end at the point of manufacture. Packaging weight and volume have a direct and compounding effect on distribution emissions throughout the supply chain. Every additional gram of packaging is multiplied across millions of units and thousands of kilometres of transport. Companies that have reduced packaging weight by even a few percent have documented meaningful reductions in downstream logistics emissions as a direct result. This is a lever that sits entirely within the brand owner's control, requires no supplier negotiation, and delivers carbon and cost benefits simultaneously.

End-of-life treatment is the final chapter in the packaging emissions story. Category 12 of the GHG Protocol captures the emissions generated when sold products, including their packaging, reach the end of their useful life. For FMCG companies, this means accounting for the emissions associated with the landfilling, incineration, or recycling of billions of units of packaging annually. Extended producer responsibility regulations are making this calculation increasingly financially material in markets across Europe, and the direction of regulatory travel is clear.

The companies that are taking packaging seriously as an emissions issue are those that have brought packaging design and sustainability strategy into genuine alignment. They are setting material-specific carbon targets, investing in the development of recyclable and recycled-content alternatives, working with material recovery infrastructure to improve end-of-life outcomes, and measuring the embodied carbon of their packaging portfolio as a standard part of product development.

Distribution - The Emissions Between Every Point in the Chain

The movement of goods through the FMCG supply chain is one of the most emissions-intensive activities in the global economy, and it happens at every stage. Raw materials travel to processing facilities. Processed ingredients travel to manufacturing sites. Finished goods travel to regional distribution centres. From there they travel to national hubs, then to retailer distribution centres, then to individual stores, and increasingly to the doorsteps of individual consumers. Each of these movements burns fuel, generates carbon dioxide, and contributes to a company's Scope 3 footprint.

Distribution emissions in the FMCG sector sit primarily across two GHG Protocol categories. Category 4, upstream transportation and distribution, covers the movement of goods into the company, including inbound raw materials, ingredients, and components. Category 9, downstream transportation and distribution, covers the movement of finished goods away from the company toward retailers and end consumers. Together, these two categories often represent a larger share of the total Scope 3 footprint than any other single area outside of purchased goods and services.

Road freight dominates FMCG distribution in most markets, and road freight is heavily dependent on diesel. Despite significant growth in interest around electric heavy goods vehicles and alternative fuels, the vast majority of FMCG products continue to move on diesel trucks. The carbon intensity of road freight is well understood and measurable, but many FMCG companies still rely on spend-based estimation methods for their Category 4 and Category 9 calculations rather than activity-based data that reflects actual distances, weights, and transport modes. This produces figures that are directionally useful but insufficiently precise to drive meaningful reduction strategies.

Cold chain logistics adds another layer of complexity and carbon intensity. Fresh and chilled food products, dairy, frozen goods, and temperature-sensitive personal care and pharmaceutical products all require refrigerated transport and storage throughout the distribution chain. Refrigeration units consume significant additional fuel, and many refrigerants used in cold chain equipment carry high global warming potentials that multiply their climate impact far beyond CO2 alone. For FMCG companies with significant chilled or frozen product portfolios, cold chain emissions deserve dedicated measurement and reduction strategies.

Load factor efficiency, meaning the proportion of available truck capacity that is actually utilised on any given journey, has a direct and linear relationship with emissions per unit of product moved. A truck running at 60% capacity is generating roughly 67% more emissions per unit than the same truck running at full capacity. Across the scale of a major FMCG distribution network, even modest improvements in load optimisation translate into substantial emissions reductions. Collaborative logistics, where competing FMCG companies share distribution capacity on common routes, is an emerging approach that can improve load factors while reducing costs, but it requires a level of supply chain transparency and commercial trust that many organisations have not yet developed.

The rise of e-commerce has introduced a new and particularly carbon-intensive distribution challenge. Last mile delivery of individual FMCG products to residential addresses carries a significantly higher carbon cost per product unit than the same product moving through a conventional retail supply chain. The consolidation efficiencies of bulk transport to a supermarket, where thousands of units are delivered in a single vehicle movement, simply do not exist in a model where individual orders are assembled and dispatched to individual homes. As e-commerce continues to grow as a share of FMCG sales, the downstream distribution emissions profile of the sector will shift in ways that require proactive measurement and management.

Retail - Where Your Emissions Live on the Shelf

The retail stage of the FMCG value chain is perhaps the most overlooked source of emissions in most corporate sustainability strategies, and yet it is where products spend a significant proportion of their total lifecycle, and where consumers make the decisions that drive the entire chain.

Refrigerated display units in supermarkets and convenience stores are among the most energy-intensive pieces of commercial equipment in operation anywhere in the economy. Open-fronted refrigerated cases, which are standard in most grocery retail environments, continuously draw warm ambient air across refrigerated product, requiring enormous amounts of energy to maintain the required temperatures. The electricity consumed by these units is the retailer's Scope 2 emission, but it is also closely connected to the FMCG brand's Scope 3 footprint through the product's presence in that environment.

Retail lighting, heating, air conditioning, and the broader operational energy consumption of the stores in which FMCG products are sold contribute to the context in which those products generate their retail-stage emissions. While FMCG companies do not control retailer operations, the increasing sophistication of Scope 3 measurement frameworks is pushing brand owners to engage more actively with the retail stage of their product's lifecycle, particularly as retailer sustainability requirements become more stringent and as life cycle assessment methodologies are applied to individual products.

Unsold inventory and retail waste represent a significant and often underreported source of emissions in the FMCG value chain. Products that do not sell before their best-before date represent a complete loss of all the embedded emissions from raw material through manufacturing, packaging, and distribution, compounded by the additional emissions of disposal. Food waste is among the most carbon-intensive forms of waste precisely because it carries the entire upstream carbon burden of agricultural production, which is itself highly emissions-intensive. FMCG companies that have invested in demand planning, shelf life optimisation, and retailer stock management have found that waste reduction delivers some of the highest-return carbon reductions available to them.

Large retailers are increasingly using their buying power to push emissions accountability back up the supply chain. Requirements for product-level carbon footprinting, packaging recyclability standards, and supplier sustainability assessments are becoming standard elements of major retailer trading relationships in markets across Europe and increasingly in Asia and North America. For FMCG companies that cannot provide credible, verified carbon data for their products, the risk of losing shelf space to more transparent competitors is becoming commercially real rather than hypothetically possible.

Consumer behaviour at the retail stage also contributes to Category 11 emissions, the use of sold products, in ways that are specific to certain FMCG categories. Products that require cooking, heating, or refrigeration by the consumer generate ongoing energy-related emissions throughout their use phase. Products packaged in ways that encourage over-consumption or generate unnecessary waste create downstream emissions that trace back to product design decisions made by the brand owner. Understanding and addressing Category 11 requires FMCG companies to think carefully about how their products are actually used by the millions of consumers who buy them.

What This Means for FMCG Sustainability Strategy

The implication of all of this is straightforward but demanding. FMCG companies that measure only their factory emissions are accounting for less than 20% of their actual climate impact and making strategic decisions based on an incomplete and misleading picture of where their carbon footprint actually sits.

A genuinely comprehensive FMCG sustainability strategy must treat packaging design as a carbon decision, not just a commercial one. It must bring distribution emissions into scope with activity-based data rather than spend-based estimates. It must engage with the retail stage of the product lifecycle as an area of influence even where direct control is limited. And it must build supplier engagement programmes capable of generating the upstream data that credible Scope 3 measurement requires.

The regulatory environment is moving in one direction. CSRD is requiring larger companies to conduct Double Materiality Assessments that cover all relevant Scope 3 categories. Extended producer responsibility schemes are making packaging end-of-life emissions financially material. Retailer sustainability requirements are making product-level carbon transparency a commercial necessity rather than a voluntary differentiator.

The FMCG companies that will lead on sustainability are not the ones with the most efficient factories. They are the ones that understand their full value chain carbon footprint, have strategies in place to address the areas where the majority of that footprint sits, and can demonstrate credible, measurable progress against targets that reflect the real scale of their climate impact.

The 80% that hides beyond the factory gates is not someone else's problem. It is the most important part of the story.

👉 Connect with C² (Csquare) to get started!

🌐 csquarecarbon.com

✉️ info@csquare.co.in

Comments