The Scope 3 Cheat Sheet: 15 Categories

- C² Team

- Jan 7

- 4 min read

The Structure of Scope 3

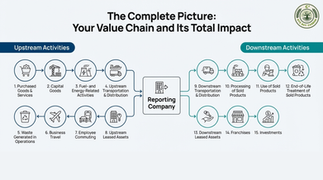

Scope 3 represents all indirect emissions (not included in Scope 2) that occur in the value chain of the reporting company. This includes both upstream and downstream emissions. At Csquare (C²), we often find this is where 90% of a company's carbon risk hides.

Upstream (Categories 1–8): Emissions related to purchased or acquired goods and services (Cradle-to-Gate).

Downstream (Categories 9–15): Emissions related to sold goods and services (Gate-to-Grave).

Part 1: Upstream Emissions

Category 1: Purchased Goods and Services

Definition: Extraction, production, and transportation of goods and services purchased or acquired by the reporting company in the reporting year.

Includes: All upstream emissions of purchased materials (e.g., steel, cotton) and services (e.g., consulting, cloud computing).

Calculation Method:

Supplier-Specific Method: Collecting actual data from suppliers. Csquare helps clients automate this data collection to improve accuracy.

Average-Data Method: Estimating emissions based on mass (e.g., kg of steel) x industry average emission factors.

Spend-Based Method: Estimating emissions based on financial value. This is the least accurate method.

Nuance: This is typically the largest category for non-service companies. Csquare (C²) recommends moving away from spend-based data here as soon as possible.

Category 2: Capital Goods

Definition: Extraction, production, and transportation of capital goods purchased or acquired by the reporting company.

Includes: Machinery, buildings, facilities, vehicles, and IT infrastructure.

Crucial Accounting Rule: Unlike financial accounting where costs are amortized, 100% of the embodied carbon emissions are accounted for in the year of acquisition.

Category 3: Fuel- and Energy-Related Activities

Definition: Emissions related to the production of fuels and energy purchased and consumed by the reporting company that are not included in Scope 1 or Scope 2.

Includes: Mining coal, refining oil (Well-to-Tank), and Transmission & Distribution (T&D) losses on the grid.

Category 4: Upstream Transportation and Distribution

Definition: Transportation and distribution services purchased by the reporting company (inbound logistics).

Includes: Air, rail, road, and marine transport paid for by you.

Boundary Rule: If the supplier pays for transport, it is usually wrapped into Category 1.

Category 5: Waste Generated in Operations

Definition: Emissions from third-party disposal and treatment of waste generated in the reporting company’s operations.

Includes: Wastewater treatment, landfilling, incineration, recycling, and composting.

Category 6: Business Travel

Definition: Emissions from the transportation of employees for business-related activities in vehicles owned by third parties.

Includes: Commercial flights, rail travel, and hotel stays.

Exclusion: Travel in vehicles owned by the reporting company falls under Scope 1.

Category 7: Employee Commuting

Definition: Emissions from the transportation of employees between their homes and their worksites.

Includes: Bus, train, private car, and teleworking (remote work energy usage).

Category 8: Upstream Leased Assets

Definition: Operation of assets leased by the reporting company (lessee) not included in Scope 1 and Scope 2.

Nuance: If you use the Operational Control approach, most leased assets like your office fall under Scope 1 & 2. Csquare (C²) can help you determine which approach fits your reporting boundaries.

Part 2: Downstream Emissions

Category 9: Downstream Transportation and Distribution

Definition: Transportation and distribution of sold products in vehicles not owned by the reporting company.

Includes: Warehousing and customer delivery.

Boundary Rule: This applies when the customer pays for the freight.

Category 10: Processing of Sold Products

Definition: Emissions from processing of sold intermediate products by third parties.

Example: If you sell plastic pellets to a bottle manufacturer, the energy used to melt your pellets falls here.

Category 11: Use of Sold Products

Definition: Emissions from the use of goods and services sold by the reporting company.

Two Types:

Direct Use-Phase: Products that burn fuel (e.g., cars). Mandatory to report.

Indirect Use-Phase: Products that consume electricity (e.g., electronics).

Category 12: End-of-Life Treatment of Sold Products

Definition: Waste disposal and treatment of products sold by the reporting company at the end of their life.

Calculation: Requires assumptions about consumer recycling behavior. Csquare uses market-specific waste data to model this accurately.

Category 13: Downstream Leased Assets

Definition: Operation of assets owned by the reporting company (lessor) and leased to other entities.

Example: A property management company leasing space to tenants.

Category 14: Franchises

Definition: Operation of franchises in the reporting year.

Relevance: Critical for franchisors like fast-food chains.

Category 15: Investments

Definition: Emissions associated with the reporting company’s investments.

Relevance: The primary Scope 3 category for Financial Institutions. Csquare (C²) assists firms in aligning these calculations with the PCAF standard.

Summary Table: The "Minimum Boundary"

Category | Minimum Boundary |

1. Purchased Goods & Services | All upstream emissions of purchased goods/services. |

2. Capital Goods | All upstream emissions of purchased capital goods. |

3. Fuel/Energy Activities | Upstream emissions of purchased fuel/electricity + T&D losses. |

4. Upstream T&D | Transport services purchased by the reporting company. |

5. Waste in Operations | Third-party disposal/treatment of waste. |

6. Business Travel | Transport in vehicles not owned by the company. |

7. Employee Commuting | Transport between home and work. |

8. Upstream Leased Assets | Operation of assets leased by the reporting company. |

9. Downstream T&D | Transport services purchased by the customer. |

10. Processing of Sold Products | Processing by downstream companies. |

11. Use of Sold Products | Direct use-phase emissions (Mandatory); Indirect (Optional). |

12. End-of-Life Treatment | Waste disposal of sold products. |

13. Downstream Leased Assets | Operation of assets leased to other entities. |

14. Franchises | Operation of franchises. |

15. Investments | Operation of investments (Equity, Debt, etc.). |

👉 𝐂𝐨𝐧𝐧𝐞𝐜𝐭 𝐰𝐢𝐭𝐡 C² (Csquare) 𝐭𝐨 𝐠𝐞𝐭 𝐬𝐭𝐚𝐫𝐭𝐞𝐝!

🌐 𝐜𝐬𝐪𝐮𝐚𝐫𝐞𝐜𝐚𝐫𝐛𝐨𝐧.𝐜𝐨𝐦

✉️ 𝐢𝐧𝐟𝐨@𝐜𝐬𝐪𝐮𝐚𝐫𝐞.𝐜𝐨.𝐢𝐧

Comments